Summarizing Q3 & What's Next for Q4

What happened in Q3 and what's on the horizon for crypto the rest of the year.

Summarizing Q3

Here’s a bullet point summary of the quarter:

The Global Liquidity Cycle will drive crypto prices higher

Phase II of the bull cycle has begun in September, a marked shift from an unspectacular summer on all fronts.

This quarter saw regulatory risk removal, which is huge long-term & for blockchain innovation

This quarter saw BTC selling pressure from ETFs, Mt. Gox, US and Germany

The market is not behaving like past post-Bitcoin Halving events, due to the crypto market more tied to the monetary cycle, which moved to accommodative from restrictive policy on September 18 with the Fed’s reduction of interest rates

GLOBAL MACRO

THE FED’S LOWERING OF INTEREST RATES KICKS OFF PHASE II

On September 18th, the Fed lowered interest rates by 50bps. The market is forecasting another 75 bps lower in interest rates over November and December. This kicks off the monetary easing cycle.

The Global Liquidity Cycle, seen above, demonstrates a clear pattern and we are now entering a period where liquidity will be pumped into the system. Global central banks need to roll their own paper, which means they need to issue new bonds to cover old bonds that are coming to maturity. Governments around the world are laden with debt. All the COVID debt issuance that happened in 2020 isn’t getting paid off, it’s getting rolled into new debt issuance, both principal and interest. It’s like a household getting a new credit card and paying the balance off of an old credit card, both the principal and all the interest accrued.

This is happening with all the top central banks around the world. The PBoC (People’s Bank of China) is getting aggressive for the first time with interest rates and money printing. The US has begun lowering interest rates and the Fed’s QT, Quantitative Tightening policy ends in Q1 2025. Famed global macro investor Raoul Pal has stated he believes the Fed will have to expand its balance sheet from the current $7T to over $12T by the end of 2025 to address all the fiscal spending required from past legislative spending. All of this is bullish for crypto.

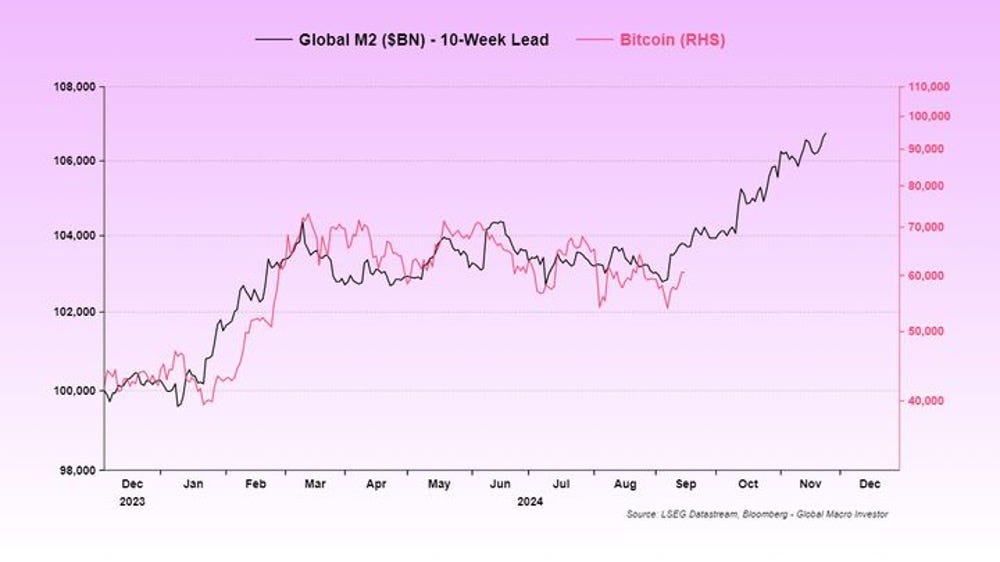

*Chart showing Global Money Supply M2 Forecasted into Q4 Overlayed with Bitcoin’s Price

Above is a chart of global M2, the world’s total money supply, forecasted 10 weeks into the future and overlayed on Bitcoin’s price. As you can see, Bitcoin’s price has closely followed the expansion of the money supply, M2 and is projected to continue.

Lyn Alden completed research that showed bitcoin’s price direction followed the money supply’s direction 83% of the time making it the clearest asset class correlated with the monetary cycle. This is key because it supports our thesis – crypto is the antidote to monetary inflation.

PAST INTEREST RATE CUTS LEAD TO HIGHER BITCOIN PRICES

In the past 3 times where interest rates were cut over the past 25 years, rates went to zero (or almost zero at 1%). In 2003, rates were cut to 1.25%, in 2008/9, rates were cut to 0%, and in 2020 rates were cut to 0%. We believe this time will be no different and rates will be cut below 2%. Consensus thinking is that rates will only be cut to 3%, but as history has shown us, some market event always happens where the Fed has justification to cut rates to close to zero (if not zero). They need to do this so that the Fed can roll all the new debt at better long-term interest rates to minimize the debt service. For every 1% in interest rates, the debt service rises $300b! So, it’s critical to central banks around the world they all get the chance to roll the debt that’s coming due at low rates. We think this time will be no different.

* Chart above showing the last interest rate cuts and bitcoin price.

As you can see in the chart above, the price of bitcoin rises quickly shortly after interest rates are cut. In 2020, rates were cut to zero and a few short months later bitcoin shot up from under $10k to over $60k in a year’s time. Then as rates were signaled to go higher, bitcoin price crashed in 2022. This was more related to Quantitative Tightening of the Fed’s balance sheet than rates per se, but both were happening simultaneously.

We suspect that both the cutting of interest rates which started on September 18th and will continue throughout 2024 and 2025 as well as the ending of QT in Q1 of 2025 will affect the price of bitcoin – to the upside. Cheaper rates allow for more credit to form and its credit that actually creates money in the system. Moreover, the Fed will begin to expand its balance sheet once again. It’s this action that is the mechanism of money printing. And, as we’ve previously stated but is worth repeating – crypto is the antidote to monetary inflation.

BITCOIN SUMMARY – SHORT-TERM BULLISH

Bitcoin was up in September +7.3% and basically flat on the quarter. Bitcoin ETFs saw inflows of $1.5b on the quarter. Throughout the quarter, we saw selling pressure from the US and German governments, selling BTC on the open markets through exchanges. Mt. Gox and FTX bankruptcies were selling assets to pay back victims. Most of this selling pressure has subsided and we expect a strong Q4.

Bitcoin achieved its all-time high (ATH) in March of this year and, while it made a couple attempts, the price has yet to break that high of $73.5k. We ended Q3 being rangebound for the quarter, with bitcoin trading in a range of $54K - $68K for all of Q3, though a new bullish trend began at the end of September. Bitcoin ended the quarter finally above its 200-day and 20-day moving averages for the first time since July.

Global macro risk is a tailwind to crypto right now with the 10-yr UST yielding 3.75% and the US dollar as measured by the DXY Index at 101. We are seeing a trend in yields falling and the USD weakening, which we forecasted, and is now creating a tailwind. The primary risk to markets now is the US election which is keeping some investors on the sidelines until after the election.

MARKET COMMENTARY

THE QUARTER IN REVIEW

In Q3 2024, the cryptocurrency market demonstrated a moderate recovery in September recovering some of the losses early in the quarter fueled by renewed institutional interest and positive macroeconomic indicators, including a more favorable inflation outlook. Ether was down -24%, and most altcoins were still down on the quarter. Regulatory scrutiny remained a focal point, particularly from the SEC, which ramped up enforcement actions against several major exchanges, leading to temporary declines in trading volumes and market confidence. Meanwhile, the decentralized finance (DeFi) sector showed signs of maturation, with the total value locked (TVL) stabilizing around $25 billion as innovative new projects focused on enhancing security and user experience. Institutional adoption also gained momentum, with prominent asset managers launching crypto investment products, indicating a shift toward mainstream acceptance.

Technological advancements in Layer 2 solutions, particularly on Ethereum, helped alleviate some scalability concerns, enabling a resurgence in decentralized applications (dApps). The NFT market saw a revival as brands engaged in high-profile collaborations, although volatility persisted, reflecting the speculative nature of the space. Geopolitical factors, including shifting monetary policies and global inflationary pressures, contributed to a growing perception of cryptocurrencies as a hedge against traditional financial instability, setting a complex backdrop for continued industry evolution.

As you can sell in the chart above, we saw mixed buying and selling pressure throughout this quarter. In Q3 2024, Bitcoin exchange-traded funds (ETFs) saw inflows totaling approximately $1.5 billion. This marked a significant increase compared to previous quarters and reflected growing institutional interest and investor confidence in Bitcoin as an asset class.

The altcoins have yet to gain steam in Phase I of this bull market, but this is to be expected. We expect alts, particularly the higher beta asses, to really shine in the final 18 months of the cycle, which we have now entered. As Phase II now begins with the Fed’s lowering of interest rates, the market will begin to see more inflow as the monetary cycle expands which will be good for crypto.

TFA Model

The MOVE Index, which tracks volatility in the bond market, is a bit high which shows liquidity issues in the UST market. That’s the main global macro risk. That’s something to watch but other than that, crypto looks bullish.

IN CLOSING

As we close out Q3, we usher in Phase II of this crypto bull market. It’s the Bitcoin Halving Event that drives Phase I and consequently bitcoin higher. Phase II is driven by the expanding monetary cycle which began on September 18th with the Fed’s 50bps rate cut. Global central banks around the world are loosening monetary policy by cutting rates. That makes credit more flowing, and more money supply created in the system. We’ll watch the global money supply, measured by global M2, expand. And with that, crypto prices rise. The Fund outperformed in September, and we think soon altcoins will start to outperform en masse.

This is a part of the 4-year cycle and its’ what drives the crypto bull market. This next 18 months is the best part of the crypto bull market from a performance standpoint. Since Chair Powell pushed for “higher for longer” rate policy, we’ve pushed back our estimate for peak-cycle to Q1 of 2026 from Q4 of 2025, and because of the shift in monetary policy we think this bull cycle is going to last longer than originally expected. We will know we’re at the end when the Fed Chair announces rate hikes and/or a return of Quantitative Tightening (QT). But between now and then, we expect another round of Quantitative Easing (QE) where the Fed uses its balance sheet to increase the money supply, aka money printing. This is what we’ve all been waiting for.

As you can see in this chart of bitcoin monthly performance, every time we’ve had a positive September, we’ve experienced the 3 consecutive months following, Q4, will all positive months. We hope this trend continues this time around. The only thing that could thwart is the US Election.

We now believe the Fed’s monetary policy is the most important factor in crypto performance. When the Fed moves to more accommodative monetary policy, through lowering rates and expanding the Fed’s balance sheet, is when we’re going to see outperformance in crypto. It’s happened every time in past expanding cycles. And this time it’s going to be even bigger because the debt continues to increase. The US national debt is now at a whopping $35.7T! At the end of 2020, the debt was just under $27T.

This time around, numbers could get truly astronomical. Famed global macro investor Raoul Pal thinks the Fed will have to expand its balance sheet from the current $7T to $12T by the end of 2025 to keep markets functioning. All that market manipulation and money printing will drive asset prices higher – stocks, bonds, gold, commodities and yes crypto. Crypto is the fastest horse in that race which is why it’s the best asset class to fight monetary inflation.

At the end of this bull cycle, the same aforementioned portfolio manager survey concluded the total crypto market cap will be close to $6T and Raoul Pal believes it will be over $10T. As the current crypto market cap is ~$2T, that’s a 3x to 5x from here. Those are truly impressive returns.

The next 6 quarters are the most important of this bull cycle. We expect Q4 to be quite positive though the election may affect performance short term. We’re hoping for an uncontested election and then 2 more rate cuts to end the year. If we get that, crypto asset performance could be substantial at the EoY.

Jake Ryan

CIO, Tradecraft Capital